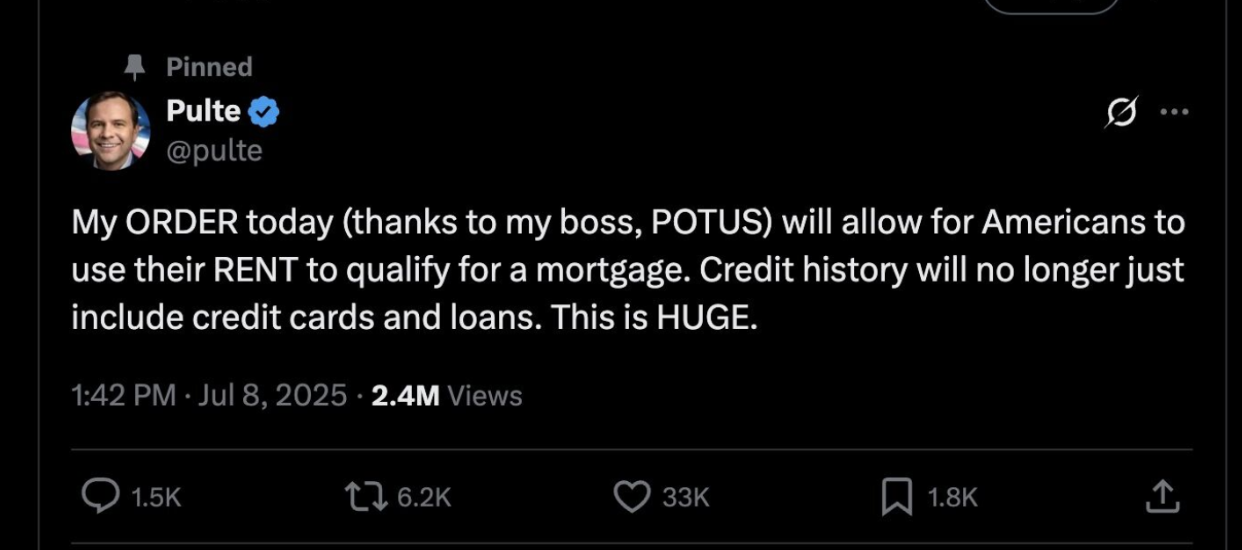

On July 10, the Federal Housing Finance Agency (FHFA) Director Bill Pulte announced a significant policy shift via X (formerly Twitter):

For millions of renters—especially those with limited traditional credit history—this update signals a potentially transformative shift in how mortgage lenders evaluate creditworthiness.

Here’s what’s actually changing, why it matters, and what to expect next.

What happened?

For the first time, mortgage lenders are now permitted to use VantageScore 4.0 in the underwriting process for loans that may be sold to or guaranteed by Fannie Mae and Freddie Mac—the government-sponsored enterprises (GSEs) that support more than 70% of U.S. residential mortgages.

VantageScore 4.0 is a modern credit scoring model that includes on-time rent payments, utilities, and other alternative data points that traditional models, such as the decades-old FICO Classic, exclude.

Previously, Fannie and Freddie required lenders to use FICO Classic from all three major credit bureaus. That model was developed in 1989 and does not account for rent history, utility bills, or other non-loan payment behavior.

Director Pulte’s announcement represents a shift from requirement to permission as lenders may now adopt a model that better reflects how today’s consumers live and pay.

Why this matters

While rent-inclusive scoring models are not new, their acceptance in the mortgage industry has lagged.

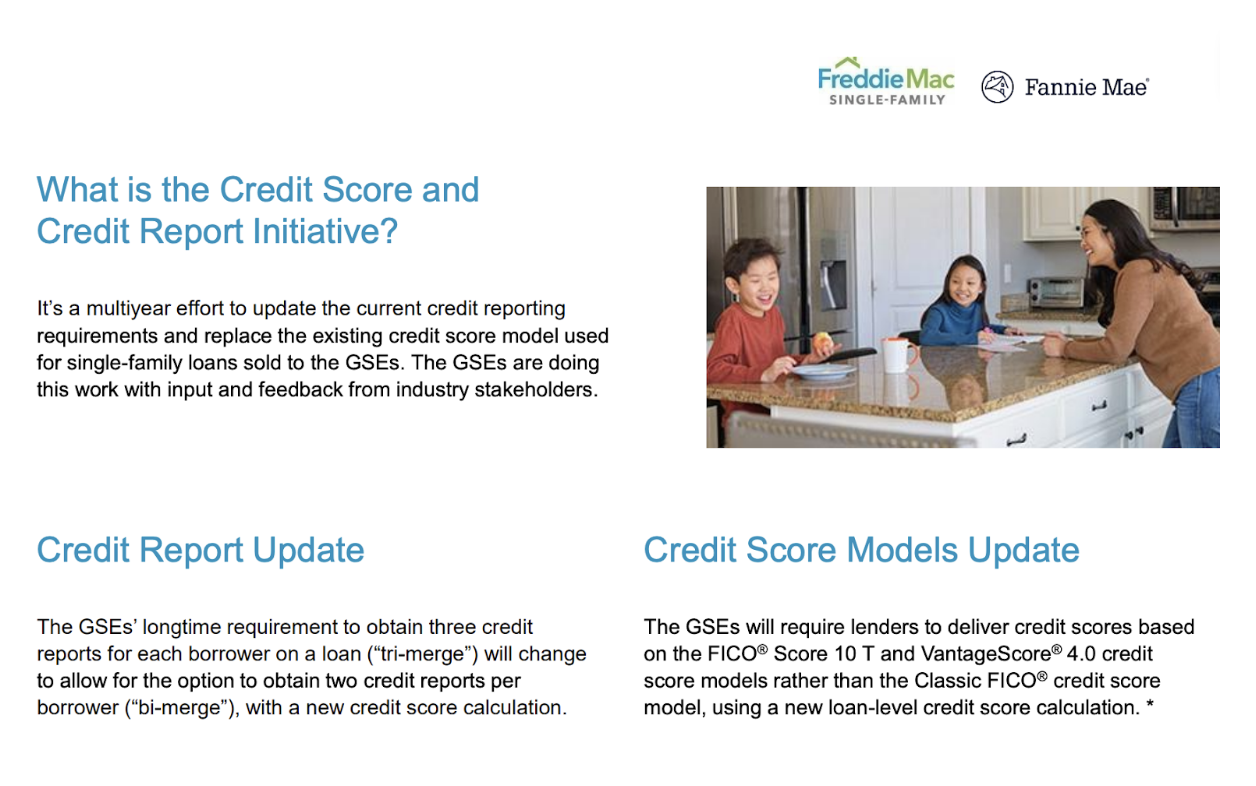

Prior to this announcement, the FHFA had already been leading a multi-year initiative to:

- Mandate the use of VantageScore 4.0 or FICO 10 T for home loans backed by Fannie Mae and Freddie Mac

- Transition from a tri-merge credit report (three bureaus) to a bi-merge model (two bureaus)

- Modernize mortgage credit evaluation by incorporating additional, predictive data

However, progress has been slow. Full implementation of the broader initiative remains a work in progress, with infrastructure, training, and system updates needed across the mortgage industry.

Director Pulte’s order accelerates the timeline by removing a key barrier: Lenders no longer have to wait.

They may begin adopting rent-inclusive credit models immediately, assuming they are operationally ready to do so.

What to watch next

The biggest question now is: Will lenders act?

Implementing a new credit model is complex. It requires internal systems changes, regulatory compliance reviews, and underwriting policy adjustments.

Some lenders, especially those with more agile infrastructure, may adopt VantageScore 4.0 sooner. Others may wait until FHFA mandates the change across the board.

However, the signal from FHFA is clear: the industry is moving toward more inclusive credit evaluation, and rent data is part of that future.

What this means for renters

While lenders consider their next move, renters can take proactive steps today.

At Boom, we’ve long believed that rent should count toward building credit. That’s why we make it easy to report your rent to all three major credit bureaus.

As rent-inclusive credit models become more widely adopted, reporting rent history can strengthen your credit profile and set you up for a better financial future when you’re ready to apply for a mortgage.

About Boom

Boom is on a mission to level the playing field for the 110+ million renters in the US by making housing more flexible, affordable, and rewarding. Boom is building a suite of rental financial services for renters and property managers, including rent payment reporting, rent reporting-as-a-service, and a number of integrations for the largest property management systems (PMS). Now serving thousands of renters, Boom is led by second-time founders Rob Whiting (ex-BCG, Rubicon) and Kirill Moizik (ex-Eco, Technion, Grubhub).