Income verification is one of the most important steps in tenant screening—and one of the most frequently done wrong. The goal is simple: confirm that an applicant can comfortably afford the unit. But the method you use to verify that income matters more than most property managers realize.

Here’s a breakdown of every major income verification method, what each one actually tells you, and where each one falls short.

Why income verification matters more than ever

More than 22 million U.S. renter households are cost-burdened, spending at least 30% of their income on housing, according to Harvard’s Joint Center for Housing Studies. Late payment rates in independently owned rentals rose from 8.8% in mid-2024 to 11.7% by June 2025.

At the same time, AI tools have made it trivially easy to generate fake pay stubs and bank statements. Relying on uploaded documents alone is no longer a reliable verification strategy.

The method you use to verify income isn’t just an administrative choice—it’s a risk management decision.

The main income verification methods

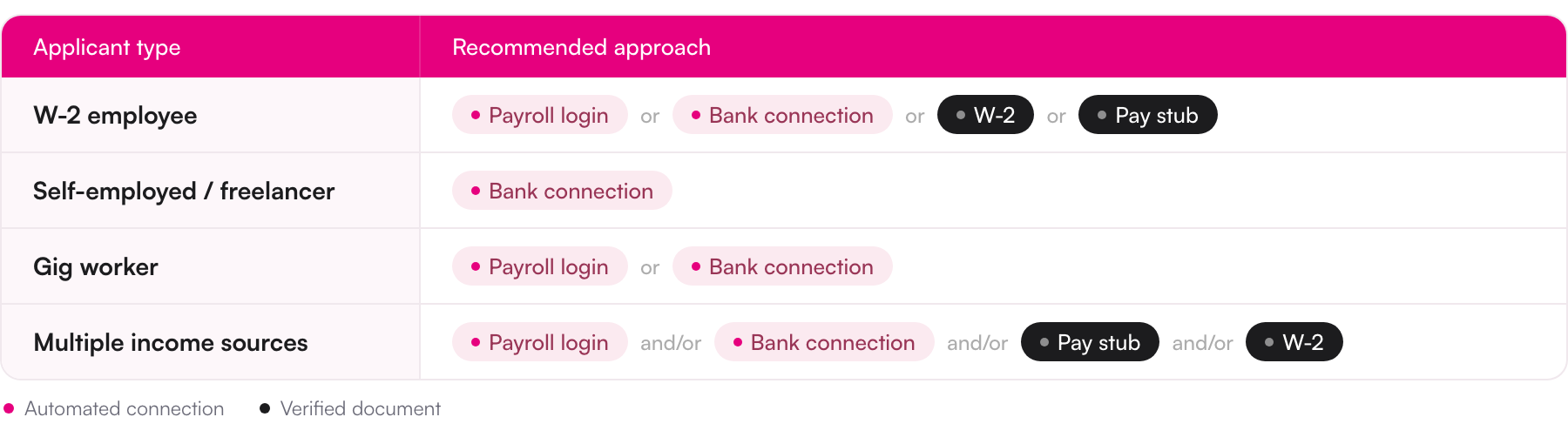

1. Pay stubs (uploaded documents)

- What it shows: Gross and net income, employer name, pay frequency, year-to-date earnings.

- What it misses: Whether any of it is real. AI-generated pay stubs are now indistinguishable from legitimate ones to the naked eye.

- Best for: Low-risk applications where other verification layers exist, or as a secondary document alongside a stronger primary source.

- Verdict: Not sufficient on its own unless paired with a platform like BoomScreen, which adds a document verification layer to catch manipulation

2. W-2s (uploaded document)

- What it shows: Annual income for traditionally employed applicants. W-2s are only applicable for employees, not self-employed applicants or freelancers.

- What it misses: Current income. A 2025 tax return tells you what someone earned last year, not whether they’re still employed or their income has changed.

- Best for: W-2 employees only. Self-employed applicants and freelancers don't receive W-2s.

- Verdict: Useful as a supplement for employed applicants, not a standalone unless paired with a platform like BoomScreen, which adds a document verification layer to catch manipulation.

3. Bank statements (uploaded documents)

- What it shows: Actual deposit patterns, recurring income, spending behavior, and account balance history.

- What it misses: Document integrity. Uploaded bank statements are among the most commonly falsified documents in rental applications. BoomScreen only accepts PDFs for bank statement uploads, which eliminates screenshots and image files as a fraud vector.

- Best for: Getting a fuller picture of financial behavior alongside other verification methods.

- Verdict: Better than pay stubs alone, but still vulnerable to manipulation unless paired with a platform like BoomScreen, which verifies bank statements to ensure that they haven't been tampered with.

4. Bank-connected income verification (via Plaid)

- What it shows: Live, direct data from the applicant's actual bank account: deposit history, income patterns, account balances, and employer deposits, pulled directly from the source with the applicant's permission.

- What it misses: Very little. Because the data comes directly from the financial institution rather than an uploaded document, there’s no document to falsify.

- Best for: Any application where income verification is a meaningful risk factor (which is most of them)

- Verdict: The most reliable method available today. Boom’s integration with Plaid brings this directly into the BoomScreen screening flow, supporting gig workers, self-employed applicants, and non-traditional income sources.

5. Payroll login (via payroll provider)

- What it shows: Live income data pulled directly from the applicant's payroll provider (Gusto, ADP, etc.) logged into via the BoomScreen application experience.

- What it misses: Only works for applicants with a payroll provider. Doesn't capture self-employed or freelance income.

- Best for: W-2 employees and gig workers with access to a payroll provider.

- Verdict: Direct from the source and nearly impossible to falsify.

What about non-traditional income?

Gig workers, freelancers, and self-employed applicants are a growing share of the renter population—and the worst-served by traditional income verification. For gig workers, pay stubs exist but don't tell the full story since income varies week to week. For freelancers and self-employed applicants, W-2s aren't even an option. This is exactly where bank-connected verification and payroll login shine: deposit patterns and direct payroll data tell the story that documents can't.

How to choose the right method

The bottom line

The best income verification method is the one that goes directly to the source. Uploaded documents—pay stubs, bank statements, tax returns—all carry some risk of manipulation. Bank-connected verification through Plaid eliminates that risk by pulling live data directly from the applicant’s financial institution.

Regardless of how applicants choose to verify their income (document upload, bank connection, or payroll login), BoomScreen verifies it and has built fraud-proof tooling to ensure accuracy at every step.